Can a price cap on Russian oil work?

REAL ECONOMY BLOG | July 18, 2022

Authored by RSM US LLP

The United States is urging its trade partners to adopt a novel proposal that would put a cap on the price of Russian oil during a time of shortcomings in global production.

It’s a creative idea, but it carries risks and could result in another surge in oil prices. Middle market firms need to understand these risks as they plan for the second half of the year.

The proposal has three objectives:

- Constrain Russia’s ability to finance its war in Ukraine.

- Prevent a further energy catastrophe in the European Union and the United Kingdom.

- Put downward pressure on global oil markets to help tame surging inflation.

To achieve the objectives, the policy would create a purchasing cartel that would limit the price of Russian oil at, say, around $40 per barrel, while not completely cutting off the flow of oil out of Russia.

But that still leaves the question of enforcement—or how to prevent Russia and other nations from getting around the cap.

The answer lies in insurance. The United Kingdom and the European Union insure somewhere between 85% and 90% of Russian oil exports. Together with the United States, they would refuse to permit the insurance of any ship that transports Russian oil above the price cap.

The U.S. government estimates that ocean-going transport ships move roughly 70% of Russia’s 5.6 million barrels a day of crude exports, with the rest sent through pipelines to Europe and China.

One approach to limiting Russian oil revenues would be to apply significant tariffs. But India and China would resist such tariffs because of the economic damage they would cause. That leaves the price cap as the most viable way to limit Russian oil revenues.

And without insurance, it would become almost impossible for Russian oil to be transported. But the approach carries risks:

- The likelihood of cheating: Like in all sanctions regimes—and this is simply a creative sanctions regime—there will be leakages and cheating given the size of Russian oil exports. The price difference between our hypothetical $40 dollar cap and the current market of around $95 per barrel is simply too great.

- The possibility that Russia acts first: Russia may choose to cut off any further oil exports to the world, which would surely send oil surging back toward recent highs near $130 per barrel.

- Distortions to the market: The policy would create further distortions in the global oil market by making it nearly impossible for commercial enterprises to hedge volatility in the market.

- The wildcard of China and India: Russia and its largest current consumers—China or India—could simply choose to create an insurance market to cover the risk of transport of Russian oil. At this time, one would think that none of the countries have the depth, breadth or global trust to create and sustain such a market, but it cannot be discounted.

Supply constraints

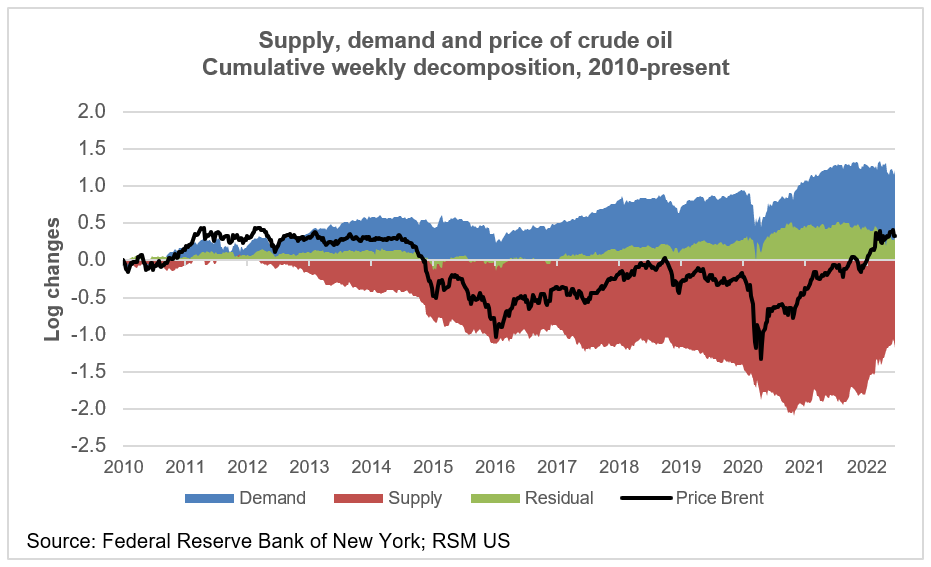

Analysis by the Federal Reserve Bank of New York found that increases in oil prices are currently more a function of anticipation of limited supplies than of overwhelming demand. The analysis found that excess supply became a significant driver of oil prices in 2012 and generally dominated price dynamics after 2014.

In the latest period, the analysis found that anticipation of decreased demand in the second quarter was offset by expectations of a greater decrease in the supply of oil. By our calculations, that resulted in the futures price of Brent crude oil increasing by 9.5% from March 31 to June 28.

Given the response of the West to the invasion of Ukraine and Russia’s threats to cut off energy supplies to Europe, the relative importance of limited supplies of oil should come with little surprise. But in terms of policy debate, the root cause of high oil prices and their effect on the inflation rate need to be accurately portrayed.

Increases oil prices are currently more a function of anticipation of limited supplies than of overwhelming demand.

For example, recent news reports suggest a misconception that OPEC can simply turn on its pumps to counter the withdrawal of Russian supplies. Even if the geopolitics were to allow production to increase, Reuters now reports it might be wishful thinking.

Saudi Arabia and the United Arab Emirates were considered to have excess capacity. But the UAE’s leader, in statements he later discounted, said that not only are the Saudis approaching their production limits, but also that UAE production is maxed out. And Libya says it might suspend exports because of its political crisis, and Ecuador’s labor strife threatens to shut down production.

This would not be the first time that concerns regarding the abundance of oil have appeared. Before the shale revolution, the debate in the early 2000s centered on “peak oil,” a theory that the world was fast running out of a finite resource.

More to the point, the concern was that peak oil supplies marked the end of cheap oil. As noted in 2014, oil is a most efficient source of energy, with a liter of diesel capable of moving tons of matter great distances at a cost less than a cup of coffee.

Policy alternatives

This brings us to policy alternatives and choices, whether or not the global producers have reached a peak. This is only the latest oil crisis brought on by a shortage of supply.

Let’s first frame the parameters of the argument. The need for fossil fuels will be around for some time.

It’s hopeless to think that the West could transition to alternate sources of energy overnight without some cost to the economy or the population. Or to sufficiently mitigate the demand for liquid fuels in order to bring down the price of energy.

Is there a policy that allows for market-based pricing of energy, with multiple sources of energy competing for market share?

As the market is set up now, oil can be extracted from a limited number of fields, with Russia one of the dominant producers. While the West hoped that Russia would join the western alliance of market-driven economies, that’s no longer realistic.

OPEC is now OPEC-plus, which includes Russia. With the supply of oil regulated by fiat or by physical restraint, price signals remain constrained.

The takeaway

Treasury Secretary Janet Yellen’s proposal to place a cap on the price of Russian oil would have a direct positive effect on large Russian clients like India and China while reducing Russia’s receipts.

In effect, that would set up a two-tiered market, with prices in Asia determined by the alliance of developed economies, and prices in the West determined by the interaction among private suppliers and consumers. But as with any market interference, there are bound to be unintended consequences.

This article was written by Joseph Brusuelas and originally appeared on 2022-07-18.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/can-a-price-cap-on-russian-oil-work/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Fitts, Roberts, Kolkhorst & Co., P.C. is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Fitts, Roberts, Kolkhorst & Co., P.C. can assist you, please contact us.